Consider this: one in three pets will require emergency veterinary treatment each year, yet only about 10% of pet owners in the U.S. have pet insurance. This immense gap highlights the importance of safeguarding your four-legged family member’s health. Pet insurance for your dog can be the safety net that ensures you’re never faced with the stress of hefty medical bills when your furry friend falls ill or gets injured.

When selecting pet insurance, several critical factors must be considered. Look for comprehensive coverage that includes accidents, illnesses, and hereditary conditions. Additionally, assess the policy’s limitations, including waiting periods and exclusions, to ensure it aligns with your dog’s specific needs. A statistic to note is that over 40% of pet owners underestimate the cost of veterinary care, making well-rounded insurance crucial for financial peace of mind.

The Importance of Pet Insurance for Your Dog

Pet insurance acts as a safety net for unexpected medical expenses. Dogs, like humans, can encounter sudden health issues or accidents. These situations can lead to costly veterinary bills. Without insurance, these expenses can be a burden. Having a good insurance policy helps alleviate financial stress.

Many pet owners underestimate the cost of veterinary care. Treatments for illnesses such as cancer or chronic conditions can amount to thousands of dollars. Pet insurance covers these unexpected costs, ensuring your dog receives the necessary treatment. This peace of mind allows you to focus on your dog’s well-being. It’s a crucial aspect of responsible pet ownership.

There are different types of pet insurance plans. Some cover only accidents, while others include illnesses and routine care. Comprehensive plans often offer coverage for surgeries, medications, and even diagnostic tests. Reviewing these options can help you choose the best plan for your dog’s needs. It’s essential to understand what each plan covers.

Insurance policies typically come with limitations and exclusions. Some may not cover pre-existing conditions or certain breeds. Reading the fine print helps avoid surprises down the road. Pet insurance can be tailored to fit your dog’s specific health requirements. This ensures you get the most value from the policy.

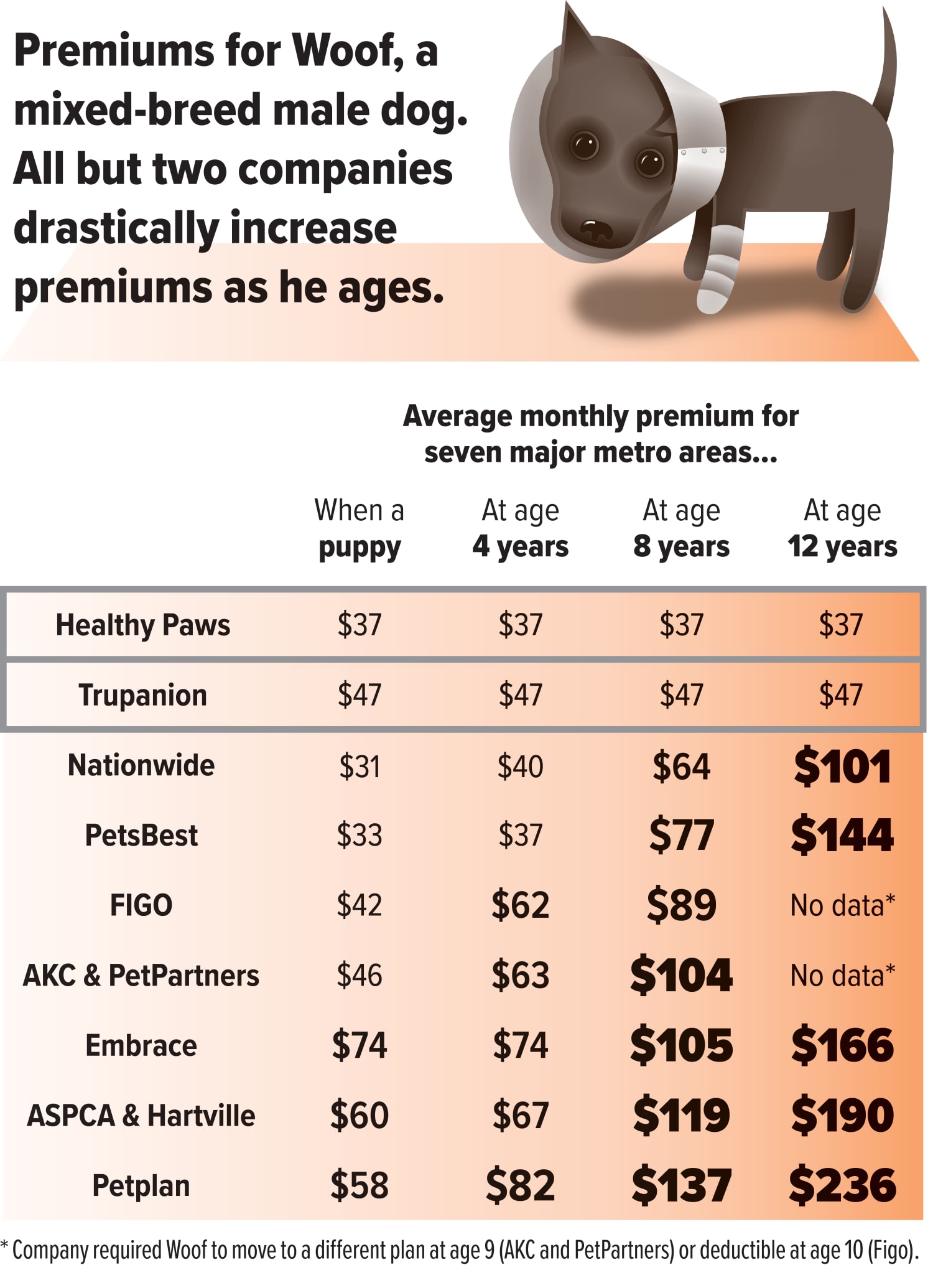

Key Statistics About Dog Health and Pet Insurance

In the U.S., only about 2.5 million pets are insured, which is a small fraction compared to the total number of pet-owning households. This shows that many dog owners are still unaware of the benefits of pet insurance. Statistics reveal that one in three pets will need emergency veterinary treatment every year, a number that highlights the importance of being prepared. Emergency treatments can be expensive, often costing hundreds or even thousands of dollars. Pet insurance can help manage these costs efficiently.

A survey found that over 40% of pet owners underestimated the cost of veterinary care. Many owners believe that routine visits cover all potential health issues, which isn’t the case. Chronic conditions like diabetes or arthritis can require long-term care and significant financial outlay. Pet insurance helps bridge this gap, covering treatments and medications that would otherwise be a financial strain. This security ensures pets receive the care they need.

According to the North American Pet Health Insurance Association, the pet insurance industry has seen a growth rate of about 23% annually in the past few years. This growth indicates an increasing awareness of the importance of pet insurance. Having a policy can provide peace of mind to owners, knowing their pets are covered in case of an emergency.

The average annual cost for dog insurance ranges from $500 to $1,000, depending on the coverage. This might seem high, but considering the potential cost of surgeries or long-term treatments, it’s a small price to pay. Investing in pet insurance ensures that financial constraints do not interfere with your dog’s health. Ultimately, it’s a step towards responsible pet ownership.

Understanding Different Types of Pet Insurance Policies

Pet insurance policies come in various forms, catering to different needs and budgets. One common type is accident-only insurance. This plan covers costs related to injuries from accidents but doesn’t cover illnesses. It’s a good option for younger, generally healthy dogs. However, it might not be sufficient for older dogs or those prone to health issues.

Another popular type is illness coverage. This type of insurance handles expenses arising from various diseases, like cancer or infections. It offers more comprehensive protection compared to accident-only plans. Many owners opt for this to ensure their pets get timely treatment for unexpected illnesses. It’s especially useful for breeds known for specific health problems.

Some policies offer wellness coverage, which includes routine care such as vaccinations, dental cleaning, and regular check-ups. Though this type of insurance costs more, it helps offset the routine expenses every pet owner faces.

For those seeking the most extensive coverage, comprehensive plans combine accident, illness, and wellness benefits. While these are the most expensive, they provide the highest level of protection. Comprehensive plans are ideal for pet owners who want to leave no stone unturned when it comes to their dog’s health. Evaluating the different options ensures you choose the best plan for your dog’s unique needs.

What to Look for in a Pet Insurance Plan

When choosing a pet insurance plan, pay attention to the coverage options. Make sure the plan covers both accidents and illnesses, as these are the most common reasons for vet visits. Some plans may only cover one or the other, so it’s essential to read the fine print. Comprehensive plans offer broader protection but may come with higher premiums. However, the extra cost could be worth the peace of mind.

Another crucial factor is the waiting period. This is the time between signing up for the insurance and when the coverage actually starts. Shorter waiting periods are preferable, as your pet will be protected sooner. Each insurer has different policies, so compare them to find the best fit. Be aware that certain conditions may have extended waiting periods.

Check if the insurance plan has any exclusions. Some policies do not cover specific breeds or pre-existing conditions. This could limit the usefulness of the plan, especially if your dog is prone to certain health issues. Always ask for a list of exclusions before making a decision. Knowing what’s not covered is as important as knowing what is.

Consider the reimbursement model used by the insurance company. Some insurers use a percentage-based model, where they cover a percentage of the vet bill. Others use a benefit-schedule model, assigning specific payouts for different treatments. Each model has its pros and cons, so choose the one that aligns best with your financial situation.

Cost is always a significant factor. Monthly premiums can vary widely based on the coverage and provider. While it’s tempting to go for the cheapest option, make sure it offers adequate protection. Sometimes, spending a bit more can save you a lot in the long run. It’s essential to balance cost with coverage.

Customer reviews and ratings can provide valuable insights. Look for feedback from other pet owners who have used the insurance. Their experiences can help you gauge the reliability and effectiveness of the plan. Checking reviews can also alert you to any common issues or hidden fees. This ensures you make an informed choice.

Navigating Policy Limitations and Exclusions

Understanding policy limitations and exclusions is key to choosing the right pet insurance. Many policies exclude pre-existing conditions, which are ailments your dog already has before the coverage starts. Knowing this can help you manage your expectations and plan accordingly. Some policies also exclude congenital or hereditary conditions. Read the policy details carefully to be fully aware of these limitations.

Exclusions could also extend to specific breeds. Certain breeds, known for particular health issues, might not be covered. For example, Bulldogs and German Shepherds are often excluded due to their predisposition to specific ailments. Make a list of common exclusions to discuss with potential insurers. This way, you can avoid unexpected surprises later on.

Policies often have limitations on coverage amounts for specific treatments. There might be annual limits, per-incident caps, or lifetime maximums. These caps can significantly influence your out-of-pocket expenses. Reviewing these limitations is crucial to ensure the plan meets your pet’s needs. To make it easier, here’s a brief table summarizing common limitations:

| Limitation | Description |

|---|---|

| Annual Limit | Maximum amount paid per year |

| Per-Incident Limit | Cap on a single incident or condition |

| Lifetime Limit | Total maximum payout over the policy’s life |

Waiting periods are another limitation. This is the time you have to wait after getting the policy before making a claim. Different policies have different waiting periods, which can vary for accidents versus illnesses. Shorter waiting periods are generally better, allowing you to start using your coverage sooner. Always check the waiting period for each insurer.

Be mindful of the fine print in policy documents. Some policies have clauses that need careful reading to fully understand. Terms like “experimental treatments” or “non-standard procedures” may not be covered. Discuss these details with insurance agents to clarify any ambiguities. Thorough understanding ensures you get the most out of your pet insurance.

Evaluating Cost and Value in Pet Insurance

Evaluating the cost and value of pet insurance involves looking at more than just the monthly premiums. Start by considering what the policy covers versus what it costs. Analyze different scenarios like accidents, illnesses, and routine care. Compare these factors to the potential expenses you might face without insurance. This will help you determine if the plan is worth the investment.

The deductible is another important aspect to consider. A higher deductible generally means lower monthly premiums, but more out-of-pocket costs when you make a claim. Understanding your financial situation can help you decide which deductible level is best. Here’s a quick comparison table:

| Deductible Type | Pros | Cons |

|---|---|---|

| High Deductible | Lower monthly premiums | Higher out-of-pocket costs |

| Low Deductible | Lower out-of-pocket costs | Higher monthly premiums |

Look at the reimbursement percentage that the insurance company offers. This is the portion of the bill they will cover after you’ve paid the deductible. Policies usually cover between 70% and 90% of eligible expenses. A higher reimbursement percentage means more financial relief in the event of a claim. However, it may also come with higher premiums.

Don’t forget to assess the annual or lifetime coverage limits. These are the total amounts that the insurance will pay out over a year or the pet’s lifetime. Plans with higher limits can be more useful for chronic conditions, which may require long-term treatment. It’s essential to balance these limits against the cost to find the best value.

Lastly, consider any additional perks or services the policy might offer. Some plans include extras like behavioral therapy, alternative treatments, or even boarding fees if you’re hospitalized. Such added benefits can enhance the overall value of the policy. Evaluating these extras alongside the basic coverage can guide you in making an informed choice.

Frequently Asked Questions

Pet insurance can seem complex, so we’ve answered some common questions to help you make an informed decision. These answers will cover the essentials, from costs to coverage options.

1. How much does pet insurance typically cost?

The cost of pet insurance varies based on factors like your dog’s age, breed, and health. On average, dog owners pay between $30 to $50 per month for standard coverage. Some high-end plans with comprehensive benefits can go over $100 monthly.

Premiums also depend on whether the plan covers accidents only or includes illnesses and wellness care. Comparing different insurers is essential for finding a policy that fits your budget while offering adequate coverage.

2. Does pet insurance cover pre-existing conditions?

Most pet insurance policies do not cover pre-existing conditions, which are health issues present before the start of coverage. This exclusion is a key consideration when choosing a plan.

If your dog has existing health problems, you’ll need to manage those expenses out-of-pocket. Some insurers offer limited coverage for these conditions after a waiting period if they become symptomatic again later on.

3. What is a deductible in pet insurance?

A deductible is the amount you pay out-of-pocket before the insurance company starts covering vet bills. Higher deductibles generally result in lower monthly premiums but mean more upfront costs when filing claims.

You can choose between annual deductibles, which reset each year, or per-incident deductibles applicable to each claim separately. Evaluating your financial situation helps determine which type of deductible suits you best.

4. Are routine check-ups covered by pet insurance?

Routine check-ups and preventive care are covered under wellness plans rather than typical accident or illness policies. Wellness plans include services like vaccinations, dental cleanings, and regular exams.

This type of coverage often requires an additional premium but offsets regular healthcare costs significantly. Reviewing the specifics of each plan ensures it fits your needs and covers these routine expenses effectively.

5. How does reimbursement work in pet insurance?

Reimbursement involves the percentage of vet bills that your insurer will pay back after you’ve paid your deductible. Common reimbursement rates range from 70% to 90%, depending on the policy chosen.

The higher the reimbursement rate, the less you pay out-of-pocket during claims processing timeframes. Be sure to understand whether reimbursements are based on actual vet bills or benefit schedules set by the insurer.

Conclusion

Choosing the right pet insurance for your dog involves careful consideration of various factors. From understanding different types of policies to evaluating costs and exclusions, making an informed decision is essential. This effort not only provides financial peace of mind but also ensures your beloved pet receives the best care possible.

Remember to review customer feedback and compare multiple plans to find the best fit for your dog’s specific needs. By taking the time to research and evaluate, you can secure a policy that offers comprehensive protection. Ultimately, a good pet insurance plan is a crucial aspect of responsible pet ownership.

Contact Off Leash K9 Training Spokane, Washington here to learn more about the Training Programs they offer to help you and your dog.

Their website: http://www.dogtrainersspokanewa.com

Phone: 509-481-9223

To Find an Off Leash K9 Training location near you look here.